Twenty One: Jack Mallers’ Blueprint for the “Ideal Bitcoin Company”

From Bitcoin Treasury Vehicle to Bitcoin Operating Company

Twenty One’s next chapter is not simply about holding Bitcoin. Jack Mallers is trying to define a new category: a publicly listed, Bitcoin-native operating company that combines treasury scale, financial services, mining infrastructure, capital markets engineering, and M&A.

That distinction matters.

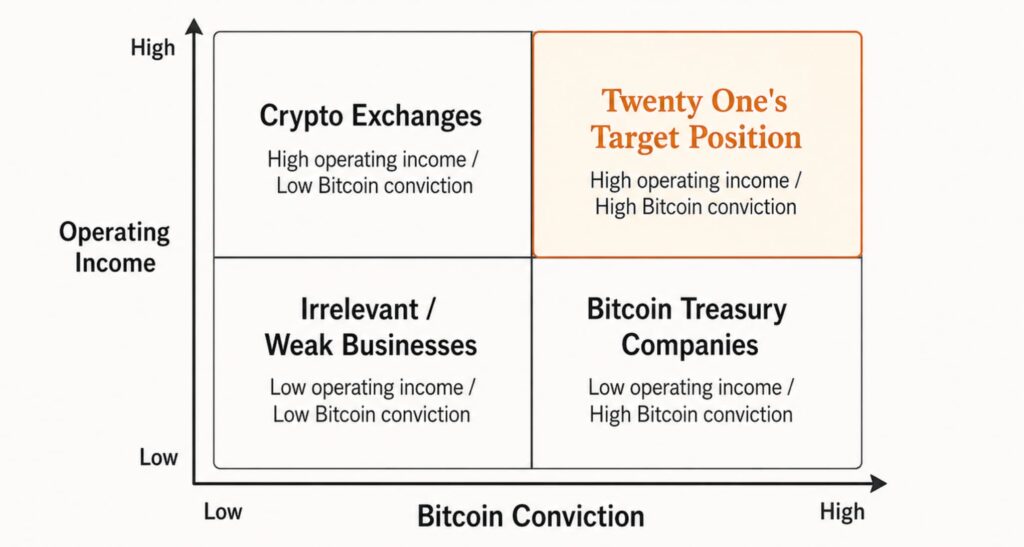

Most public Bitcoin companies today fall into one of two buckets. On one side are crypto exchanges: high operating income, massive distribution, deep product breadth, but often diluted Bitcoin conviction. On the other side are Bitcoin treasury companies: high Bitcoin conviction, strong capital markets execution, but limited operating income and limited direct product distribution.

Jack’s idea is that the ideal Bitcoin company should sit in the top-right quadrant: high Bitcoin conviction and high operating income. In his words, 21 should not become a “crypto casino,” nor should it remain only a Bitcoin treasury company. It should become a full-stack Bitcoin company.

The Core Thesis: Bitcoin Conviction + Operating Cash Flow

The key insight from Jack’s keynote is that Bitcoin conviction alone is not enough.

A company can hold Bitcoin, issue equity, issue convertibles, buy more Bitcoin, and grow Bitcoin per share. Strategy and Metaplanet have already shown how powerful that model can be. But Jack’s critique is that this model is still largely capital-markets-led. It depends heavily on market access, equity premiums, investor demand, and BTC volatility.

Twenty One’s proposed evolution is different. The company wants to pair a large Bitcoin balance sheet with actual Bitcoin-native businesses that generate revenue and cash flow. That operating layer could reduce dependence on common equity issuance over time.

Tether Investments has proposed merging Twenty One with Strike and then with Elektron Energy, creating a single public company combining Bitcoin treasury holdings, Bitcoin financial services, and large-scale Bitcoin mining infrastructure.

This is the institutional significance: Jack is not pitching Twenty One as “another MSTR.” He is pitching it as a Bitcoin conglomerate.

Jack’s Four Pillars of the Ideal Bitcoin Company

1. Bitcoin Financial Services

The first pillar is a global financial services arm.

Strike is central to this vision. Jack describes Strike as a kind of global Bitcoin bank, while being clear that it is not legally a bank. The platform already offers Bitcoin buying and selling, withdrawals, direct deposit, bill pay, Bitcoin-backed loans, and a Bitcoin line of credit.

This matters because financial services create two forms of value.

First, they generate operating revenue. Lending, custody, brokerage, payments, and credit can become recurring business lines.

Second, they create distribution. A Bitcoin company with millions of financial services users has an advantage that a pure treasury company does not. It can originate loans, custody collateral, distribute structured products, onboard Bitcoiners, and convert user relationships into recurring revenue.

In Jack’s framework, this is what separates a Bitcoin operating company from a passive Bitcoin holder.

2. Bitcoin Infrastructure and Mining

The second pillar is physical Bitcoin infrastructure.

Through the proposed Elektron Energy transaction, Twenty One would gain exposure to industrial-scale Bitcoin production. Tether’s announcement describes Elektron as a large-scale Bitcoin mining platform that would add mining infrastructure, operational depth, and execution capabilities to the combined company.

Jack described Elektron as having roughly 50 exahash across the platform, representing approximately 5% of the Bitcoin network, according to the keynote transcript.

Strategically, this is important because mining gives Twenty One a potential source of internally generated Bitcoin. Instead of only buying BTC through capital markets, the company could also produce Bitcoin through infrastructure.

That creates a more vertically integrated model:

energy → mining infrastructure → Bitcoin production → treasury growth → capital markets products

For a Bitcoin company, this is powerful because it links operational execution directly to balance sheet growth.

3. Capital Markets

The third pillar is capital markets engineering.

This is where Twenty One starts to look most interesting from an institutional investor’s perspective.

Jack’s idea is not merely to issue common stock and buy Bitcoin. He specifically raised the possibility of using preferred stock, convertible bonds, structured products, fixed-income products, and securitization. In the keynote, he discussed securitizing mining revenue, lending books, and other Bitcoin-native cash flows.

This is the bridge between Strategy’s model and a broader Bitcoin capital markets model.

Strategy pioneered the idea that a Bitcoin balance sheet can be used to issue different securities for different investor appetites: common equity, convertibles, preferreds, and other instruments. Twenty One’s potential edge is that it may eventually have operating cash flows underneath those securities.

That is the key difference.

A pure treasury company finances itself primarily against the market’s willingness to value Bitcoin exposure at a premium. A Bitcoin operating company could finance itself against treasury assets and operating cash flows.

That makes non-dilutive growth more realistic over time.

4. Mergers and Acquisitions

The fourth pillar is M&A.

Jack wants Twenty One to acquire profitable Bitcoin companies and strategic Bitcoin assets. In institutional language, this means Twenty One could become a consolidation platform for the Bitcoin economy.

This is a very important point.

If Bitcoin adoption continues, there will be a long tail of Bitcoin-native companies across payments, custody, lending, mining, infrastructure, wallets, data, and financial products. Many of these companies may be profitable but subscale. Twenty One could use its public currency, Bitcoin balance sheet, and capital markets access to acquire them.

That creates a compounding flywheel:

Bitcoin balance sheet → public market valuation → acquisition currency → more cash flow → stronger capital markets access → more Bitcoin accumulation

This is not a passive treasury strategy. This is a roll-up strategy built around Bitcoin.

Why Jack Rejects the “Crypto Casino” Model

A major part of Jack’s argument is ideological.

He contrasts his vision with crypto exchanges and platforms that monetize speculation across tokens, prediction markets, trading activity, and casino-like behavior. His critique is not that these businesses are bad financially. In fact, he acknowledges that crypto exchanges can be extremely profitable businesses. His issue is that they are not necessarily high-conviction Bitcoin companies.

This is why the Coinbase comparison matters in his quadrant framework. Jack argues that a company can generate high operating income but still have low Bitcoin conviction if its core business is broadly crypto rather than Bitcoin-specific.

Twenty One is meant to be different.

It is designed to be Bitcoin-only, or at least Bitcoin-first in the strongest possible sense. That positioning may reduce product breadth, but it increases brand purity, ideological clarity, and alignment with Bitcoin-native investors.

For public markets, this creates a differentiated investor proposition: not “crypto beta,” but Bitcoin operating leverage.

Why Jack Also Distances Twenty One from Pure Treasury Companies

Jack also makes a second distinction: Twenty One should not be seen merely as a Bitcoin treasury company.

This is striking because Twenty One holds one of the largest corporate Bitcoin positions in the world. CoinDesk reported that Twenty One entered the market as a Bitcoin treasury firm with 43,514 BTC, backed by Tether, Bitfinex, and Jack Mallers.

Yet Jack’s point is that holding Bitcoin is only the starting point.

A treasury company’s core question is:

How do we grow Bitcoin per share through capital markets?

Jack’s ideal Bitcoin company asks a broader question:

How do we build operating businesses that serve Bitcoiners, produce Bitcoin, generate cash flow, and use capital markets to compound the entire system?

That is a much bigger ambition.

In this sense, Twenty One is not rejecting the Strategy playbook. It is trying to extend it.

Strategy proved that Bitcoin can become a corporate treasury reserve asset and that capital markets can be used to grow Bitcoin exposure. Twenty One wants to add financial services, mining, securitization, and M&A on top of that foundation.

The Strategic Logic of Combining Twenty One, Strike, and Elektron

The proposed three-way structure has a clear strategic logic.

Twenty One contributes the public company shell, Bitcoin treasury, institutional investor base, and capital markets platform.

Strike contributes the operating financial services business, global distribution, regulatory infrastructure, and Bitcoin-native product engine.

Elektron contributes Bitcoin production capacity, mining infrastructure, and physical exposure to the Bitcoin network.

Tether’s proposal explicitly frames the transaction as a way to accelerate Twenty One’s strategic direction by combining Strike’s profitable financial services platform with Elektron’s mining infrastructure.

For investors, the combined entity would be more complex than a pure Bitcoin treasury company, but also potentially more durable.

The model would have three sources of Bitcoin-related value creation:

- Balance sheet appreciation from BTC holdings.

- Operating income from financial services and mining.

- Capital markets accretion through structured financing and potential M&A.

That is why Jack calls it the ideal Bitcoin company.

The Institutional Bull Case

The bullish case for Twenty One is that it could become the first true public Bitcoin operating conglomerate.

If successful, it would have several advantages:

First, it would have a large Bitcoin treasury from day one.

Second, it would have a Bitcoin-native financial services distribution engine through Strike.

Third, it would have Bitcoin production capacity through Elektron.

Fourth, it would have access to public capital markets, allowing it to issue securities, acquire companies, and structure Bitcoin-linked products.

Fifth, it would have ideological clarity: Bitcoin only, not crypto casino.

That combination could make Twenty One a unique public market vehicle. Investors would not just be buying Bitcoin exposure. They would be buying exposure to the buildout of Bitcoin financial infrastructure.

In a mature version of the thesis, Twenty One becomes something like:

a Bitcoin bank + Bitcoin miner + Bitcoin treasury company + Bitcoin capital markets platform + Bitcoin M&A vehicle

That is a much more ambitious model than simply “hold BTC and issue stock.”

What Investors Should Watch

The opportunity is large, but execution risk is also meaningful.

The first thing investors should watch is whether the proposed mergers actually close and on what terms. The strategic vision is compelling, but deal structure, dilution, governance, and integration will matter.

The second thing to watch is Strike’s financial profile. If Strike is profitable and scalable, it materially changes Twenty One’s quality. If its profitability is thin or volatile, the story remains more dependent on BTC and capital markets.

The third thing to watch is mining economics. Elektron’s value will depend on hashprice, energy cost, uptime, capex needs, and BTC price. Mining can be powerful, but it is cyclical and operationally demanding.

The fourth thing to watch is whether Twenty One can issue capital without destroying Bitcoin per share. Jack’s stated ambition is to use cash flow and potentially non-dilutive leverage, but the market will judge the company by whether financing decisions are accretive or dilutive over time.

The fifth thing to watch is whether the company can maintain Bitcoin purity while scaling. The temptation for any financial platform is to expand into broader crypto speculation because it can be profitable. Jack is explicitly rejecting that path. Investors should hold the company accountable to that positioning.

Final Takeaway

Jack Mallers’ idea of the ideal Bitcoin company is not a passive treasury vehicle and not a crypto exchange.

It is a vertically integrated Bitcoin-native operating company with four pillars:

financial services, mining infrastructure, capital markets, and M&A.

Twenty One’s ambition is to sit in the top-right quadrant: high Bitcoin conviction and high operating income. That is the core of Jack’s thesis. A company that only holds Bitcoin has conviction but limited operations. A crypto exchange has operations but diluted Bitcoin purity. Twenty One wants both.

If Strategy created the blueprint for the Bitcoin treasury company, Jack is trying to create the blueprint for the Bitcoin operating company.

The market may initially value Twenty One based on its BTC holdings. But if Jack executes, the long-term story will not be about how much Bitcoin Twenty One owns today. It will be about whether Twenty One can become the public-market operating layer for the Bitcoin economy.